We have all had this conversation — or been in it ourselves.

Someone smart, successful, and financially aware explains why they haven’t started investing yet. The market feels too high right now. There’s an election around the corner. The global situation looks uncertain. They’ll start in a few months, once things settle down.

A few months pass. Something else comes up. The cycle continues.

What looks like careful planning is actually one of the most costly financial habits an Indian investor can have. Not because the concerns are wrong — some of them are perfectly reasonable. But because waiting for the perfect moment to invest has a real, measurable price tag. And most people never find out what it costs them until it’s too late to do anything about it.

The Perfect Moment Has Never Arrived — And It Never Will

Here is the uncomfortable reality: there has never been a time in history when markets looked completely safe. Not in 2003. Not in 2010. Not in 2020. There was always a reason to wait.

And yet, an investor who put ₹10,000 into the Indian market in 2001 and simply stayed invested earned an annualised return of 15.61% through to 2025. Not by picking the right stocks. Not by timing market cycles. Simply by staying.

“The market’s best days don’t send a calendar invite. They arrive without warning — and almost always right after the worst days. The investor waiting on the sidelines for safety is the one most likely to miss them entirely.”

The COVID-19 crash of March 2020 is perhaps the clearest example in recent memory. The Sensex fell more than 38% in a single month. Every headline screamed disaster. Every instinct said: get out, wait for clarity, invest when things stabilise.

What happened next? The Nifty 50 rallied over 105% from its March 2020 low to February 2021. The investors who stayed — or who had the courage to invest through the panic — doubled their money in under a year. The ones who waited for clarity missed the entire recovery.

Let’s Put a Number on It — What Waiting Actually Costs

This is where it gets very real.

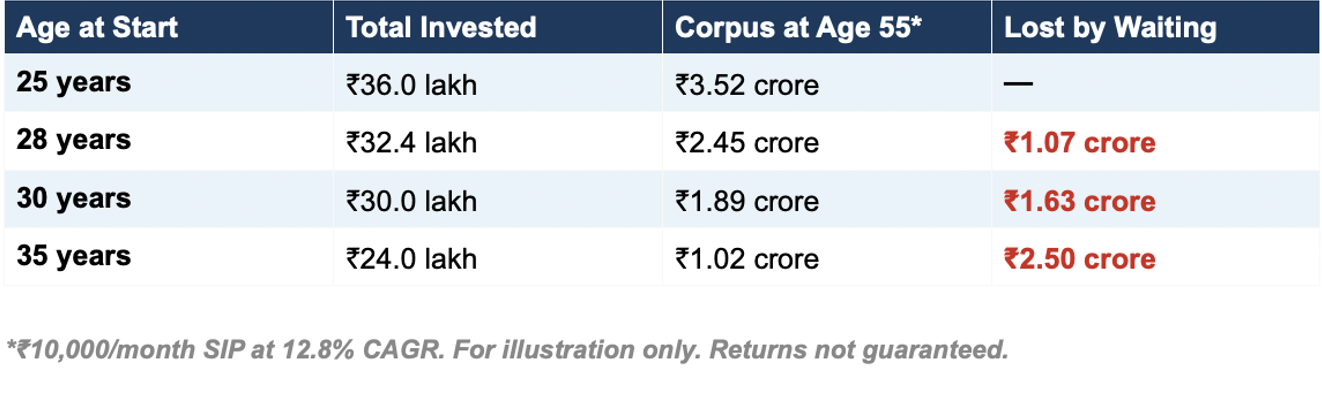

Imagine two people — both 25 years old, both planning to invest ₹10,000 every month, both targeting retirement at 55. One starts today. The other waits just three years and starts at 28 instead.

The one who waits invests only ₹3.6 lakh less in total over their lifetime. That doesn’t sound like much, right?

“But at the Nifty 50’s long-term CAGR of 12.8%, that three-year delay costs ₹1.07 crore in the final retirement corpus. Over one crore — lost by waiting just three years.”

Why such a dramatic difference? Because the first few years of a SIP are the most valuable. The money invested at 25 has 30 years to compound. The money invested at 28 has only 27. Those three years at the beginning — when the amounts are smallest — end up generating some of the largest returns of the entire journey.

This is what compounding does. It doesn’t reward patience. It rewards early action.

Why Do We Keep Waiting, Even When We Know Better?

This is the question worth sitting with. Most people who delay investing are not lazy or careless. Many of them read about markets, follow the news, and genuinely intend to start. So why don’t they?

The honest answer is that our brains are wired to see waiting as a sensible, responsible act. It feels like we are being careful. But in the context of long-term investing, it is the opposite. Here’s why:

- We remember the bad times too vividly. After a market crash, our minds expect another one soon. We’ve just seen prices fall — so we wait for them to fall further before getting in. But the second fall often never comes. Or it comes three years later, by which time we’ve missed a significant rally.

- Losing money feels worse than missing gains. Research shows that the pain of a financial loss feels about twice as intense as the pleasure of an equivalent gain. So we stay out of markets to avoid the fear of loss — not realising that staying out is itself a guaranteed, slow-motion loss to inflation.

- Waiting feels productive. Saying “I’m waiting for the right time” feels like a decision. It feels like we’re in control, being strategic. But in reality, it’s often just a comfortable way to avoid the discomfort of committing.

- We’re waiting for certainty that doesn’t exist. Some investors believe they’ll invest once things ‘settle down.’ But markets don’t settle down. Uncertainty is a permanent feature of investing — not a temporary phase that passes before the real opportunity begins.

Stopping Your SIP Is Equally Costly

The waiting problem isn’t only about people who haven’t started. It also shows up — sometimes more expensively — in the behaviour of investors who have already started a SIP and then pause it during a market fall.

Here’s what the data shows: six pauses of just three months each across a 20-year SIP — motivated by short-term worry — reduce the final corpus by approximately ₹8 to ₹12 lakh. Each pause seems small and temporary. Together, they are anything but.

“When markets fall, your SIP is buying more units at lower prices. Stopping it at that moment is like walking away from a sale just as the discounts get deepest.”

The simplest protection against this is automation. An automated SIP doesn’t give us the option to pause emotionally. It keeps investing through the noise — which is precisely what builds wealth over the long run.

So When Is the Right Time?

The answer is both simple and a little anticlimactic: as soon as possible, with a plan that fits your life — and then without stopping.

This doesn’t mean jumping in blindly. It means accepting that there will never be a moment when all the signals are green and the path feels completely safe. That moment doesn’t exist. It has never existed. The investors who have quietly built significant wealth in India are not the ones who found the perfect entry point. They are the ones who started, stayed consistent, and did not let fear override discipline.

Markets will always give us a reason to wait — a budget announcement, an election, a global conflict, a valuation concern. These are not obstacles to investing. They are the permanent backdrop against which investing has always happened.

How Bigwallet Prime Wealth Helps You Stop Waiting and Start Building

Most investors don’t need more information. They need someone to help them act on what they already know.

Bigwallet Prime Wealth is a SEBI-registered Mutual Fund Distributor and wealth management company that works with everyday Indian investors to close the gap between intention and action. Our role is not just to recommend funds — it is to help you build a plan you will actually stick to, through good markets and bad.

- We build a plan around your life, not the market. We start by understanding your goals — when you want to retire, what your child’s education will cost, whether you want to buy a home. From there, we build an investment plan designed around those timelines, not around market conditions.

- We help you stay invested when it feels hardest. The most valuable thing we do is not pick the right fund. It is helping you not stop your SIP in March 2020, or in October 2022, or the next time markets correct. That discipline is worth more than any fund selection.

- We set up automated SIPs so emotions don’t get a vote. An automated SIP removes the need to make a decision every month. It invests through volatility, through corrections, and through the moments when every instinct says to stop.

- We review your portfolio regularly — but without panic. We conduct structured portfolio reviews to ensure your investments remain aligned with your goals. What we don’t do is react to every market movement. Long-term planning requires long-term perspective.

- We explain everything clearly, always. We believe you should understand exactly where your money is going and why. An investor who understands their plan is far more likely to stay the course when markets get uncomfortable.

The investors who build real wealth are not the ones who found the perfect moment. They are the ones who started, had a plan, and had someone by their side when the temptation to stop was strongest.

The Bottom Line

Waiting for the perfect time to invest is not caution. It is a cost — one that compounds quietly against you with every passing month.

A three-year delay costs over a crore in your retirement corpus. Pausing your SIP six times costs lakhs you can never recover. And the best market days — the ones that do the most for long-term wealth — arrive without notice and leave the same way.

Markets will never be perfect. Conditions will never be ideal. The right time to invest is not a point on a chart. It is a decision you make, and then keep making, regardless of what the headlines say.

The right time to invest was yesterday. The second-best time is today. The cost of waiting one more day is small. The cost of waiting one more year is not.

By Isha Abhay Patil at BigWallet Prime Wealth

***Disclaimer: This article is for educational purposes only and does not constitute investment advice. Mutual fund investments are subject to market risks. Please read all scheme-related documents carefully before investing.

References:

- ProfitNifty — Nifty 50 Historical Returns: What Your SIP Becomes in 10-20 Years (April 2026).

- Belong — Market Timing vs Staying Invested: What the Data Says (January 2026).

- My ETF Journey — When Is the Best Time to Invest? The Data-Backed Answer for 2026.

- Gavhale, S. (2025). F&O Expiry vs. First-Day SIPs: A 22-Year Analysis of Timing Advantages in India’s Nifty 50. D Y Patil International University.

- Schwab Center for Financial Research — Does Market Timing Work? Analysis of 1926-2021 Investment Data.

- NSE India — Nifty 50 Index Historical Performance Data.